Facing a financial audit can be daunting, but a well-prepared company can navigate the process smoothly. This comprehensive guide provides a checklist to help you prepare for a financial audit, ensuring a smooth and successful outcome.

A financial audit is a formal examination of a company’s financial records by an independent third party. This process validates the accuracy and completeness of financial statements, ensuring compliance with accounting standards and regulations. Understanding the key steps in preparing for an audit is crucial to a successful outcome.

The first step in preparing for a financial audit is meticulous record-keeping. All financial transactions must be documented accurately and chronologically. This includes invoices, receipts, bank statements, and any supporting documents. Organize these documents in a clear and systematic manner.

Establish a clear understanding of the specific requirements and procedures outlined by the auditor. Review the audit scope and any particular areas of focus. The auditor will usually provide specific instructions for the company’s preparation.

Ensure your accounting procedures are up to date and compliant. Internal controls play a vital role in preventing errors and fraud. Strong internal controls help safeguard assets and maintain the accuracy of financial data. Review internal controls and procedures to ensure they align with best practices.

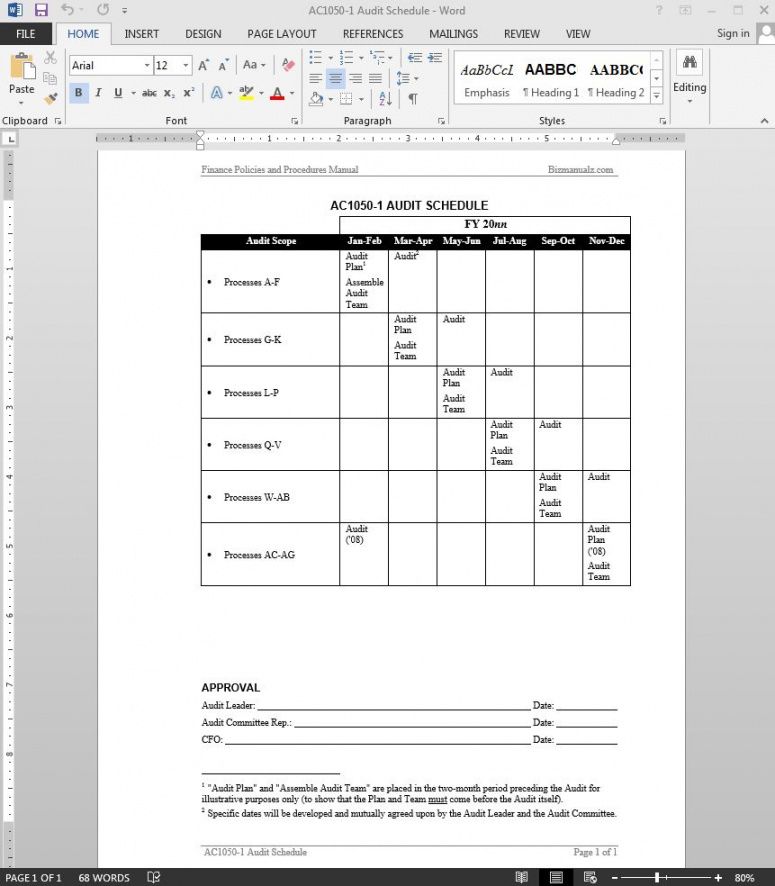

Gather and organize all necessary financial documents. This includes general ledgers, trial balances, balance sheets, income statements, cash flow statements, and any other pertinent records.

Train your accounting team on audit procedures and expectations. Familiarity with the audit process is vital. Your team must understand the auditor’s role, the scope of the audit, and their responsibilities.

Confirm that your accounting software and systems are in good working order and compliant with relevant accounting standards. If necessary, consider updating software or systems to meet the needs of the audit.

Conduct a thorough review of financial transactions. Look for any discrepancies, errors, or irregularities that might affect the accuracy of the financial statements. This step requires careful attention to detail.

Ensure all financial statements are accurate and comply with generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS). Inaccurate or incomplete statements will delay the audit and can cause issues further down the road. A professional accountant can help you ensure accuracy and compliance with the rules of accounting practices, specifically during the preparation stage before the audit takes place. Use a professional to check your accuracy as often as possible. Double check everything and double check again and again until everything is correct and aligned with accounting standards to reduce the possibility of errors and omissions when the auditor does their review and verification steps, especially with financial statements. Ensure all financial statements accurately and honestly reflect the financial position of the company, as these are core to the audit process. Remember that your financial records are a reflection of your business, and maintaining a meticulous record and proper accounting practices will significantly ease the audit process overall and help ensure compliance with all accounting rules and standards in the auditing phase. Make sure all documents follow accounting standards so there are no discrepancies during the audit period, as this can also delay and potentially create errors during the audit process, with the audit process’s core goal being the verification and validation of all financial statements. A thorough knowledge of all accounting processes and procedures is key to a successful audit preparation process. This is especially true in order for you to know and be aware of any potential problems or issues that may come up during the audit process. By proactively addressing issues and ensuring accuracy, you can ensure a smooth process during the audit itself. This should be a priority during the preparation phase of the audit itself. Proactively addressing these issues ahead of time can help prevent further complications during the audit process, allowing you to successfully manage the audit and achieve successful outcomes overall. Ensure all financial statements reflect the company’s true financial position, and that everything is in accordance with the accounting standards as this will ensure that the financial documents are in line with the GAAP and IFRS standards and prevent further errors and complications during the audit process. This also reduces the potential for errors during the audit process. By having all records and documentation aligned and prepared correctly from the beginning, you can minimize errors or disputes with the auditor and ensure a successful audit outcome as well as success in the long run for the entire company. Review any accounting procedures, methods or practices and revise them if necessary to meet the standards and procedures of accounting practices, especially if the company’s accounting practices may potentially violate specific rules and standards of accounting practices. Be fully and clearly transparent with the auditor. Transparency in all aspects of your company’s finances will be beneficial during the audit process. Be transparent to reduce the potential for errors and increase the possibility for success in the audit process, because if something were to be found incorrectly or lacking by the auditor, you want to ensure that you can clearly address the issue correctly and successfully. You don’t want to delay the audit process by having any missing records, so transparency in all documents is important. If there is a discrepancy or potential issue in your company’s accounting practices, ensure that you take action and address the issue immediately. Immediately addressing the discrepancy will help and improve the audit process and prevent delays during the audit phase. By addressing the issues at the early stages of the preparation, the audit process can be successfully navigated and handled, ensuring you have a successful and seamless audit experience from the beginning to the end. Don’t be afraid to seek help from an accounting professional if you’re unsure about any aspect of your financial records. Be very open and transparent with the auditor and ask any questions you may have regarding the audit process or the documents they need to review. Maintaining the right posture and a great attitude during the process is key to a successful outcome and will give you the most successful result possible, as a good relationship with your auditor will also improve the success of the audit process in the long term. Make sure you comply with all GAAP or IFRS accounting standards and regulations, and accurately and completely disclose all your assets, liabilities, and equity to ensure compliance. Ensure there are no omissions or inaccuracies in these disclosure sections. Maintain strong internal controls, and create and maintain proper financial recordkeeping throughout the entire process to reduce the risk of errors and enhance accuracy in all financial statements, and keep documentation up to date, accurate and complete. Be prepared to answer any questions about your accounting procedures or financial records thoroughly and completely during the audit process, being open and honest and forthcoming to the auditor will help make the process more efficient. Be open and honest and provide any documentation and information requested by the auditor during the audit process to prevent delays and complications during the audit phase itself. Having all your documents and records organized and readily available will make the entire process much more straightforward and smoother to go through. Also, maintain accurate financial records and keep them up-to-date consistently for the entire year and beyond to improve the audit process and maintain your financial standing in the best possible manner possible. Don’t be afraid to seek help from an accounting professional to help and support you, as they can help you with any questions that you may have regarding the accounting practices or other documents that are involved in the auditing preparation stage. This also applies when making sure you have all the necessary documents for the audit process. Maintaining a consistent record-keeping process will prevent delays, issues, and errors from happening during the audit process, making it a much more successful experience and smooth audit process overall. Using accounting software can also help with the record-keeping, making it consistent and readily available, increasing efficiency and accuracy. This also helps in preventing any mistakes or omissions that may occur during the process, keeping the process consistent and smooth. These steps will improve the audit process for all involved and help increase the likelihood of success throughout the process, from beginning to end. This includes maintaining all financial documents up to date for the entire audit year and beyond. Maintaining updated financial documentation for the entire year and beyond will make sure everything is clear and accurate throughout. Maintaining the accuracy and completeness of all records and financial statements is important for ensuring a smooth and effective audit process from beginning to end. A smooth and well-run audit process benefits all involved parties and improves efficiency greatly when all documents are kept accurate, in order, and in one consistent location. The benefit of organized records and documentation will reduce the possibility of mistakes and errors during the audit process. Ensuring everything is well organized, up-to-date and completely organized will lead to a more accurate and complete audit process. This helps to reduce the number of issues during the audit process. Keep documentation accurate, organized and available throughout the process in one consistent location. By following these steps, maintaining accuracy in all financial records, and staying updated, you can improve efficiency and increase the possibility of a successful audit process.

Preparing for a financial audit requires a proactive and organized approach. By meticulously reviewing your financial records, understanding audit procedures, and ensuring your team is prepared, you can confidently navigate the audit process and minimize any potential issues. Remember, proactive measures save time, money, and stress in the long run.