Depreciation and amortization are fundamental concepts in accounting, impacting how businesses report and manage their assets. While they might sound similar, they represent distinct processes with key differences in application and impact.

Understanding the nuances between depreciation and amortization is essential for accurate financial reporting in accounting. Both methods allocate the cost of assets over their useful lives, but they differ significantly in their application.

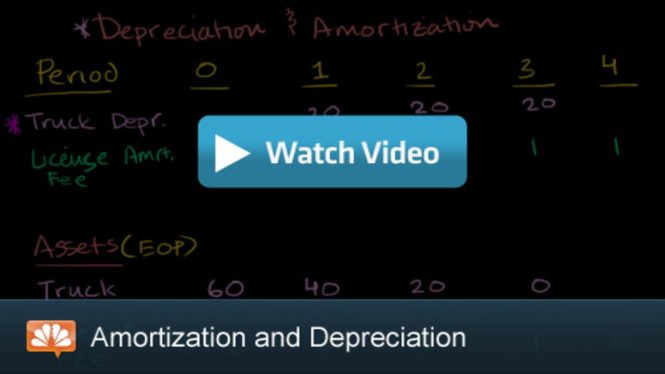

Depreciation primarily concerns tangible assets, like machinery, equipment, and buildings. It reflects the decrease in the asset’s value due to wear and tear or obsolescence over time. Conversely, amortization applies to intangible assets—patents, copyrights, and trademarks—and represents the systematic expensing of their value over their useful lives.

Different depreciation methods exist, each with its own implications. Straight-line depreciation is straightforward, spreading the cost evenly over the asset’s useful life. Accelerated methods, such as declining balance, recognize higher depreciation expense in the early years of an asset’s life. Choosing the appropriate method depends heavily on the asset’s characteristics and the business’s accounting policies.

Amortization, like depreciation, also follows various methods. Straight-line amortization is common, but other methods, like the units of production method, reflect the asset’s actual usage. The selection process involves assessing the asset’s expected economic benefits throughout its lifespan and making sure the chosen method accurately reflects this.

The choice of depreciation and amortization methods has profound effects on a company’s financial statements. Higher depreciation expense in the early years, for example, might lead to lower reported profits initially, but it also reduces taxable income over time. Likewise, understanding the implications of different amortization methods on the income statement is crucial.

Accounting principles dictate the guidelines for both depreciation and amortization. Consistency and adherence to established standards are critical. Companies must document their chosen methods and demonstrate their appropriateness. Non-compliance with generally accepted accounting principles (GAAP) can lead to significant issues.

Tax implications are another key aspect to consider. Depreciation and amortization can significantly reduce taxable income, leading to tax savings. However, the methods chosen must conform to tax regulations, which sometimes differ from accounting practices.

The complexity in depreciation and amortization extends to asset impairments. If the fair value of an asset falls below its carrying amount, impairment must be recognized in the financial statements. This process, governed by accounting standards, is crucial for a realistic representation of the asset’s worth.

In conclusion, understanding depreciation and amortization is not just about calculating numbers; it’s about accurately reflecting the financial realities of a company’s assets. By grasping these concepts, businesses can make more informed decisions regarding investment strategies and financial planning, ensuring long-term success and stability. Proper application of these methods contributes to the trustworthiness and reliability of financial statements, crucial for stakeholders’ confidence and decision-making in the business world.

In conclusion, understanding depreciation and amortization is crucial for accurate financial reporting and informed decision-making in accounting. By grasping the nuances of these methods, businesses can better manage their assets, predict future financial performance, and make strategic investments.